Does M2 drive the price of gold?

People love a clean story: the Fed prints, the dollar weakens, gold goes up. Simple. Comforting. Wrong in the way that most comforting stories are wrong.

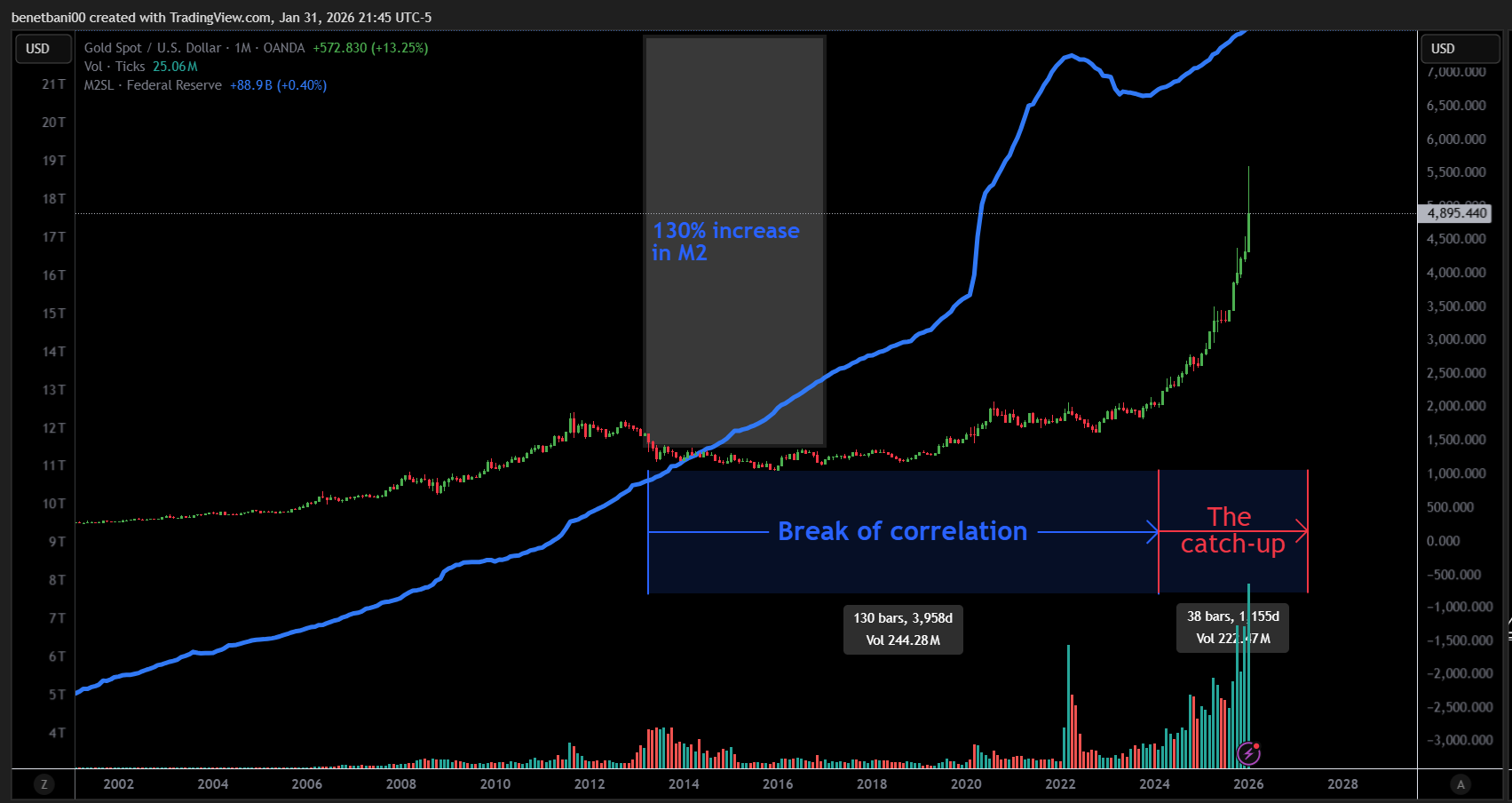

Gold is not a day trader’s instrument. It is not a monthly scoreboard for central-bank sins. It is more like a slow-learning but serious student: it eventually catches up, but it takes its time, and it refuses to follow your calendar.

Let’s start with what is true.

Gold is priced in dollars, and the dollar has been losing purchasing power for more than a century. So yes, over long periods, expanding money supply and persistent currency debasement are part of the backdrop. If you widen the lens far enough, gold tends to reflect that backdrop.

The part investors mess up is the timing. They want gold to behave like a leading indicator, a clean signal you can front-run. They want to plug M2 into their brain, press a button, and get a trade.

That is where the data gets messy, because the market is messy.

Month to month, gold is a poor narrator of “money printing.” It reacts to a cocktail of forces that have nothing to do with your favorite macro chart: positioning, fear, calm, liquidity, and something most people underestimate, real interest rates.

Real rates are simple in concept: the return you get after inflation. If cash and short-term bonds pay you a decent real return, holding gold feels expensive, because gold does not pay you anything. If real rates are negative or collapsing, gold suddenly looks less like a dead rock and more like an insurance policy.

Now add the dollar. When the dollar strengthens, gold often struggles. Not because gold became worse, but because the measuring stick changed. A stronger dollar can make gold look expensive to the rest of the world, which matters because gold is global. That alone can overpower the “printing” narrative for long stretches.

Here is the uncomfortable bit.

Even if your long-term thesis is right, gold can be “wrong” for five to ten years. Overvalued or undervalued relative to broad money growth, and it can stay there long enough to make you question your sanity.

That is not a bug. That is the feature.

Markets do not pay you for being right. They pay you for being right at the right time, with the right sizing, and with enough patience to survive boredom and regret.

Stop for a second.

If you buy gold because you think money printing is an immediate catalyst, you are not buying insurance. You are trading a narrative. And narrative trades break people, because narratives do not come with a timetable.

Let me make this concrete.

Imagine it is a year where headlines scream “printing,” “stimulus,” “debt,” “currency collapse.” You buy gold expecting a clean upward line. Instead, gold chops sideways for months. Then it drops 15 percent because yields rise and the dollar strengthens. Your friends tell you gold is dead. You sell. Two years later, gold recovers and then pushes higher, not because it listened to your original chart, but because the macro mix finally shifted back in its favor.

What broke you was not the thesis. What broke you was the mismatch between thesis horizon and portfolio behavior.

This is where most $50k to $1M portfolios get quietly damaged. Not by one catastrophic bet, but by repeated medium-sized bets built on stories that were not meant to be traded.

Gold’s role is not “make me rich next quarter.” Gold’s role, when used properly, is “help me not get wrecked if the measuring stick keeps shrinking.”

That is a different job. Different expectations. Different sizing.

There is also a second trap: fake diversification.

People tell themselves they are diversified because they own stocks, some ETFs, some gold, maybe a bit of crypto, maybe a commodity fund. Then a real liquidity event hits and everything sells off together, because when leverage unwinds, correlation goes to one. Gold can hold up better than many risk assets in some stress periods, but it is not a guaranteed shield in every panic, especially if the panic is “sell what you can.”

Liquidity is the risk lens most retail investors ignore. If you own gold through a product that is thin, expensive, or hard to trade, it can fail you when you need it most. Not because gold failed, but because your wrapper failed.

So where does that leave a sane investor?

With rules of thumb, not fantasies.

Treat gold like long-duration insurance, not a trading trigger. If your reason for buying gold is “Fed printed this month,” you are setting yourself up for disappointment.

Match the holding period to the thesis. If you believe gold follows broad money growth with multi-year delays, then you are signing up for multi-year patience. If you cannot stomach that, do not pretend you can.

Size it so it cannot bully your portfolio. The classic mistake is going from “I want a hedge” to “I am all-in on the hedge.” Concentration risk does not disappear just because the asset is shiny.

Watch the drivers that actually move gold in the short to medium term: real rates and the dollar. You do not need a PhD for this. If cash starts paying you real yield again, gold usually has a harder time. If the dollar rips higher, gold often fights uphill. These forces can dominate for long stretches.

Separate conviction from timing. You can believe gold is undervalued relative to money growth and still accept that the catch-up may take years. The market is allowed to be early, late, and rude.

Do not use leverage on a patience trade. Leverage turns time into your enemy. If the gap can last five to ten years, leverage can wipe you out long before “eventually” arrives.

Use rebalancing, not prediction. If gold is part of your risk system, rebalance around it. Add when it is hated and cut when it is loved, within predefined bands. This is not glamorous. It works because it forces you to act against your emotions.

If you want one sentence that captures the whole point: gold is not a lie detector for money printing, it is a slow mirror for currency credibility.

And slow mirrors are psychologically brutal. They do not reward urgency. They punish impatience. They make you sit with ambiguity, which is exactly what most investors cannot tolerate.

So here is the open-ended question I think investors should ask themselves before they touch gold.

Are you buying gold because you want a hedge against long-term monetary decay, or because you want a quick win that proves you are smarter than the headlines?

The answer determines whether gold helps your portfolio or becomes another expensive lesson.

Disclaimer: This is educational commentary, not financial advice. I do not know your situation, and you should make decisions based on your own research and professional guidance.